The climate sector may have wasted a decade underinvesting in nuclear because it was culturally unpopular, while simultaneously overfunding software layers that could never solve baseload energy constraints alone.

For years, nuclear sat outside the acceptable narrative of climate tech. Too expensive. Too political. Too slow. Too risky. Now, many of the same investors and operators who once avoided the category are re-entering the conversation aggressively, not because sentiment has changed, but because the underlying assumptions about energy demand and infrastructure have broken.

The Structural Shift: How AI Altered Energy Demand Assumptions

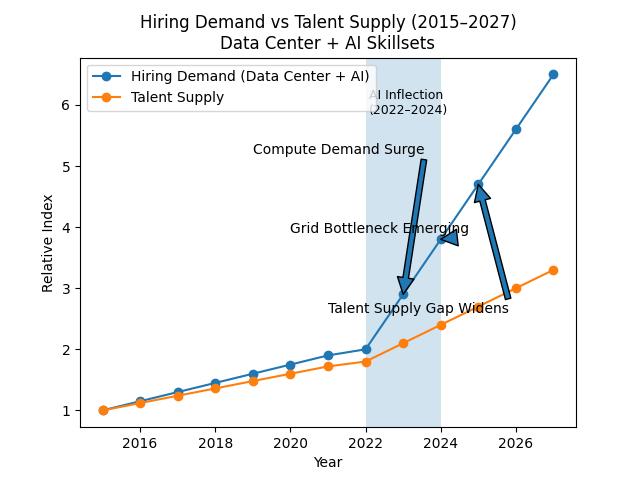

AI has fundamentally changed energy demand assumptions. Until recently, the industry operated under the belief that demand would grow incrementally and could be met through a combination of renewables, storage, and efficiency gains. That framework is no longer holding. The scale and consistency of power required to support AI infrastructure, data centers, and next-generation compute has introduced an entirely new category of demand, one that is continuous, high-density, and increasingly time sensitive. This is not just an increase in load; it is a structural shift in how energy is consumed, where it is needed, and how quickly capacity must be deployed.

What makes this moment particularly important is that it forces a reassessment of what types of energy systems can realistically support the next phase of growth. AI infrastructure does not tolerate intermittency in the same way other forms of demand can. It requires reliable, always-on power at scale, often in close proximity to compute clusters and industrial hubs. As a result, the conversation is moving beyond how to decarbonize existing demand and toward how to build new energy infrastructure fast enough to support what is coming next. This is where nuclear energy, alongside broader energy infrastructure, is being pulled back into focus.

The Reality of Grid and Baseload Infrastructure Constraints

The reality is that infrastructure constraints have now caught up with the market. For years, there was an implicit assumption that renewable energy, paired with battery storage and software optimization, would be sufficient to meet growing global energy demand. In practice, that assumption is proving incomplete. Baseload power requirements, grid reliability, transmission bottlenecks, and interconnection delays are not being solved at the pace required, particularly as demand accelerates across AI, electrification, and industrial systems. This is not a failure of renewable energy, but a reflection of the scale and complexity of replacing legacy energy systems with intermittent generation alone.

Beyond Legacy Hardware: The Evolution of Advanced Nuclear Technology

At the same time, nuclear technology itself has evolved in ways that many in the climate and venture ecosystem have not fully accounted for. The category is no longer defined solely by large, capital-intensive, decades-long projects. A new generation of advanced nuclear companies is rethinking how nuclear is designed, financed, and deployed. Advances in small modular reactors (SMRs), simulation software, advanced materials, modular construction, and AI-enabled operational systems are fundamentally changing what is possible.

Companies such as Oklo, TerraPower, X-energy, Kairos Power, Zap Energy, and emerging players like Nuclearn AI are approaching nuclear with a systems-level mindset that integrates software, modeling, and operational intelligence from the outset. This is not a return to legacy nuclear. It is the emergence of a new category of energy infrastructure, one that is computationally designed, modularly deployed, and increasingly optimized through software.

The Software Layer: Enabling Next-Gen Physical Infrastructure

This is where the narrative has shifted in a way that is often misunderstood. Software is not being displaced. It has become the enabling layer for a new generation of physical infrastructure. It allows nuclear systems to be simulated before they are built, optimized in real time, and integrated into increasingly complex energy networks. What was once a purely hardware-driven industry is now defined by the intersection of energy systems, software, AI, and advanced engineering.

This shift is also reflected in where capital is moving. Investor ecosystems that have historically backed frontier technologies, including Founders Fund, DCVC, Andreessen Horowitz, Lowercarbon Capital, and Breakthrough Energy, are actively deploying capital into nuclear energy, advanced reactors, and energy infrastructure platforms.

As investors at DCVC have articulated, solving climate at scale requires working on “the hardest, most capital-intensive problems,” not just the fastest-moving ones. Breakthrough Energy has similarly emphasized that achieving net-zero will depend on technologies capable of delivering reliable, scalable power, not incremental efficiency gains alone.

This is not opportunistic interest. It is a recognition that solving climate, energy security, and industrial growth requires engaging with complex, long-duration infrastructure investments.

Rebuilding and Acceleration: The Future of Climate Tech Investment

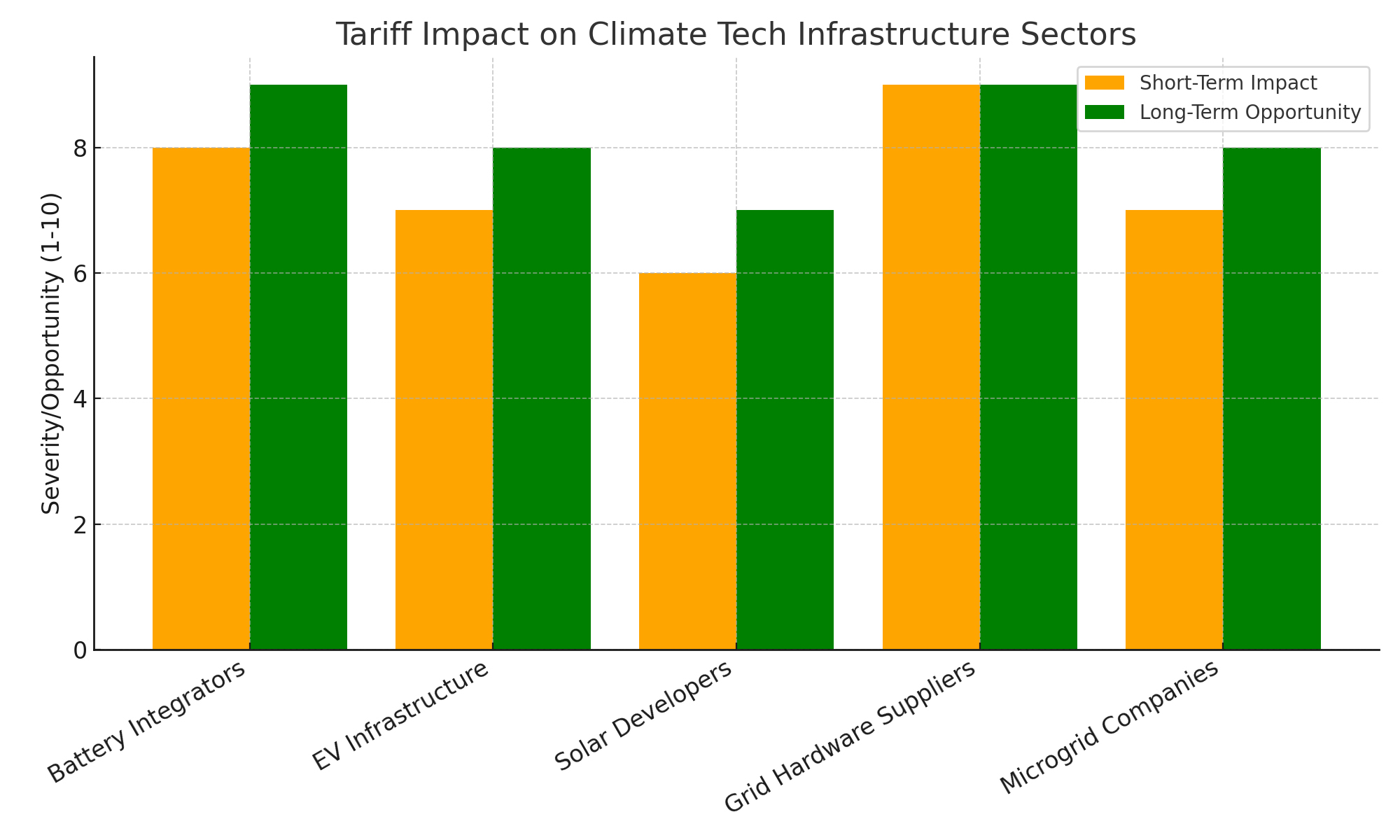

The more controversial reality is that the market is not simply rediscovering nuclear. It is correcting for a period of underinvestment driven as much by narrative as by technical or economic constraints. Capital flowed aggressively into software-defined climate solutions that could move quickly, while foundational energy infrastructure, including nuclear, was deprioritized due to perceived risk and political sensitivity.

That imbalance is now being exposed.

Nuclear is no longer being evaluated solely as an energy category. It is increasingly being evaluated as critical infrastructure for the AI era, global energy security, and industrial resilience.

The question is no longer whether nuclear belongs in the climate conversation.

It is whether the industry can move fast enough to rebuild the capabilities it chose to overlook.